hankyoreh

Links to other country sites 다른 나라 사이트 링크

[Special report] Chaebol heads at the root of the problem

By Kwak Jung-soo, senior staff writer

“…the prime cause of the discount is more likely to be poor corporate governance at the family-run chaebol conglomerates that dominate the economy.” The Economist, Feb 11th 2012

“Weaker corporate governance is one reason, among others, why Korean . . . firms tend to have lower margins than many of their international peers.” Fitch ratings agency, Feb. 24, 2012

The damaging effects of South Korean conglomerate (chaebol) malfeasance are being noticed internationally. The UK economic news magazine The Economist and Fitch, one of the world‘s top three credit rating organizations, recently fired broadsides at the Korea discount, referring to the lower stock values for South Korean businesses compared to foreign companies in the same sectors.

CEO irregularities and poor decisions are made at companies in more developed nations, too. Why is it, then, that risks associated with conglomerate heads are drawing worldwide attention as a crucial factor behind the Korea discount?

At companies in advanced countries, a faulty CEO is replaced. But at South Korean conglomerates, the head of a conglomerate wields absolute authority and is not replaced no matter how grievous his mistakes are.

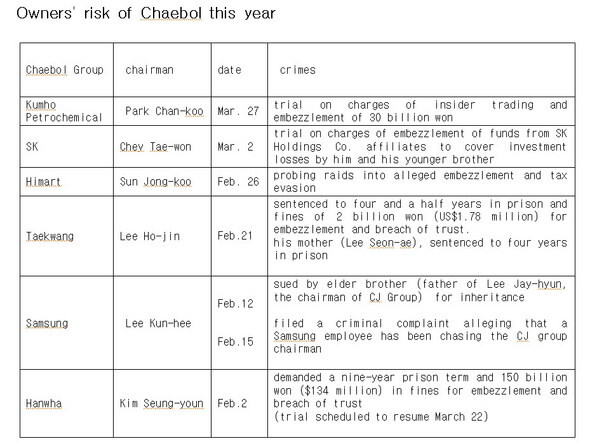

SK group, Korea’s third largest chaebol in terms of asset value, saw a high-profile embezzlement where family members of owner Chey Tae-won embezzled funds to make up for futures investment losses. In connection to that case, an SK senior executive said, “Someone within the company should be preventing the use of money from the same fund by individuals and corporations, since it could give rise to misunderstandings, but no one has taken on that preventative role.” SK

A number of other factors are cited as amplifying the risk. In terms of the corporate governance structure, there is the board of directors‘ lack of independence, along with weak monitoring and controls by shareholders.

Lee Ji-su, an attorney at the Center for Good Corporate Governance, explained that the boards of directors that are supposed to be the top decision-makers lack independence because they are staffed with people favored by the conglomerate owner.

“The external board of directors system was introduced to improve the governance structure, but now people are saying that it’s toothless,” Lee said.

As far as factors outside the company are concerned, the lack of a strong mergers and acquisition market in Korea, which means there is virtually no threat to management authority, while organizational investors like the National Pension Fund are failing to perform their role. Another factor cited was the prevalence of slap-on-the-wrist punishments from prosecutors and courts for violations of the law by conglomerate heads, as well as presidential pardons and reinstatements for businessmen.

Reflecting this situation, rankings put South Korea near the bottom of international transparency rankings. Transparency International gave South Korea 5.4 points out of 10 on its 2011 Corruption Perceptions Index, which it released in Dec. 2011. This put the country 43rd out of 183 countries examined. It was the same score the country received in 2010, but it dropped four places on the rankings from 39th to 43rd. South Korea‘s CPI has dropped steadily since President Lee Myung-bak came into office in February of 2008.

As this year’s general and presidential elections draw near, opposition parties are making plans for economic democratization and chaebol reform. Their specific objectives are to end the culture of wealthy corporate criminals being found innocent or pardoned of their crimes. The opposition parties hope this will eliminate the risks associated with chaebol heads.

The Democratic United Party (DUP) and the Unified Progressive Party (UPP) have drafted policies to improve corporate governance structures and increase monitoring of and checks on markets. The UPP has suggested increasing the independence of boards of directors by introducing a system of independent external directors to replace the outside director system, which has been described being composed of “yes-men” and “rubber stampers”.

The UPP also suggested boosting systems of participation by workers in management and employee stock-sharing plans. This is aimed at increasing the power of workers and keeping chaebol heads in check. The DUP is promoting measures including introducing multiple lawsuits against CEOs, easing requirements on class actions, expanding corporate disclosure and increasing shareholder meetings, and easing requirements allowing minority shareholders of listed companies to exercise their rights, in order to prevent tyranny by major shareholders.

“In order to allow more people to take part in shareholder meetings, [companies] should be made to reveal agendas three to four weeks in advance, rather than the current two weeks, and to introduce mandatory electronic voting so that minority shareholders can participate using social media,” said Kim U-chan, professor at KDI School of Public Policy and Management.

Many take the view that owner governance structures, in which chaebol heads wield absolute authority, must be improved if the risk posed by the heads is to be eliminated. Examples of this include tightening regulations regarding the holding company systems to increase minimum stakes in subsidiaries and sub-subsidiaries from the current 20% to 40% (40% to 60% in the case of unlisted companies), or introducing a system of a mandatory bid rule like in the UK. The mandatory bid rule system makes it mandatory for majority shareholders who acquire a stake of at least 30% to buy the shares of other shareholders at the highest price they paid their own. This could make it harder for chaebol to increase their numbers of subsidiaries using small stakes, thereby leading them to concentrate on their main areas of business.

It is not necessary to oppose the owner management system unconditionally just because of the serious risk posed by chaebol owners. Both owner management and manager management have their advantages and drawbacks. Typical examples of successful owner management include Hyundai-Kia Motors Group‘s growth into the world’s fifth largest automaker through chairman Chung Mong-koo‘s bold overseas investment and quality control-oriented management, and Samsung’s growth into a global IT power under the leadership of Lee Kun-hee.

Experts point out that owner management is most advantageous in the early stages of a company‘s establishment, but that its drawbacks are increasingly exposed as control passes to the second and third generations of owner families. “Incompetence and corruption on the part of heads are the weakest link in Korea’s chaebol system today,” said Kim Gi-won, professor at Korean National Open University.

“Founders are outstanding managers, but second and third generations are not born with genes that give them managerial ability, so they don‘t inherit it. When they take over management, their abilities have not been proven either. It is therefore highly likely that they will meet with crises in a rapidly changing managerial environment,” said Park Yoon-bae, President of Seoul Investment, a private equity firm.

English historian and philosopher Lord Acton once pointed out, “Power tends to corrupt, and absolute power corrupts absolutely.” As long as we fail to eliminate the risks associated with their heads, the chaebol’s owner management system will be hard to sustain.

Please direct questions or comments to [englishhani@hani.co.kr]

Editorial・opinion

![[Editorial] Yoon must halt procurement of SM-3 interceptor missiles](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/child/2024/0501/17145495551605_1717145495195344.jpg "[Editorial] Yoon must halt procurement of SM-3 interceptor missiles") [Editorial] Yoon must halt procurement of SM-3 interceptor missiles

[Editorial] Yoon must halt procurement of SM-3 interceptor missiles![[Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/original/2024/0430/9417144634983596.jpg "[Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis") [Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis

[Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis- [Column] Can Yoon steer diplomacy with Russia, China back on track?

- [Column] Season 2 of special prosecutor probe may be coming to Korea soon

- [Column] Park Geun-hye déjà vu in Yoon Suk-yeol

- [Editorial] New weight of N. Korea’s nuclear threats makes dialogue all the more urgent

- [Guest essay] The real reason Korea’s new right wants to dub Rhee a founding father

- [Column] ‘Choson’: Is it time we start referring to N. Korea in its own terms?

- [Editorial] Japan’s rewriting of history with Korea has gone too far

- [Column] The president’s questionable capacity for dialogue

Most viewed articles

- 1Months and months of overdue wages are pushing migrant workers in Korea into debt

- 2At heart of West’s handwringing over Chinese ‘overcapacity,’ a battle to lead key future industries

- 3[Editorial] Yoon must halt procurement of SM-3 interceptor missiles

- 4Fruitless Yoon-Lee summit inflames partisan tensions in Korea

- 5Trump asks why US would defend Korea, hints at hiking Seoul’s defense cost burden

- 6Dermatology, plastic surgery drove record medical tourism to Korea in 2023

- 71 in 3 S. Korean security experts support nuclear armament, CSIS finds

- 8[Editorial] New weight of N. Korea’s nuclear threats makes dialogue all the more urgent

- 9South Korea officially an aged society just 17 years after becoming aging society

- 10[Column] For K-pop idols, is all love forbidden love?