hankyoreh

Links to other country sites 다른 나라 사이트 링크

Korean won likely to rise in value in mid- to long-term

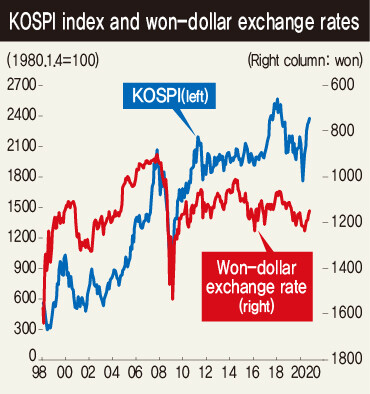

The won-to-dollar exchange rate has recently dropped to the 1,140-1,150 range after reaching as high as 1,286 last March. An examination of the factors determining the rate suggests a strong possibility that a rise in the won’s value will continue into the intermediate and long terms. Historically, stock prices have also risen when the won has increased in value.

Analysis of past statistics shows the key factors determining the won-to-dollar exchange rate to include the value of the dollar, the yuan-to-dollar exchange rate, the difference in real rates of interest between South Korea and the US, and South Korean’s current balance of accounts. To begin with, the dollar’s value has fallen by around 10% compared with the currencies of other major economies since February, and is seen as very likely to fall further as imbalances in the US economy are corrected. In two economic crises since 2008, US policy authorities have responded with bold fiscal and monetary policies to overcome them. The result has been an increase in internal and external imbalances.

As of the second quarter of this year, total US federal government debt had reached 135.6% of gross domestic product (GDP), compared with 62.9% in 2007. The fiscal deficit also stood at 15.3% of GDP as of the second quarter -- its highest rate since 1960. At 3.5% of GDP, the current balance deficit for the second quarter was its highest since 2008, when it reached 4.3%. These internal and external imbalances could be resolved through rising interest rates and a decline in the dollar’s value. With the Federal Reserve’s Board of Governors having decided to introduce “average inflation targeting,” the chances of an interest rate hike in the near future are low. For this reason, a resolution of internal and external balances through a drop in the dollar’s value appears inevitable.

If the value of the dollar declines, the relative values of other currencies are likely to rise -- one of them being the Chinese yuan. The reason has to do with the US’ rising trade deficit with China. As of last year, the US’ trade deficit with China has reached US$5.15 trillion since 2001, when China joined the World Trade Organization (WTO). Even with the US imposing tariffs to regulate imports, the deficit has remained at a high level in 2020, reaching US$193.1 billion as of August. In terms of the Chinese economy itself, the yuan’s value is likely to rise as the country’s intermediate- to long-term growth focuses on consumption and other domestic demand rather than exports. The won-to-dollar exchange rate moves in conjunction with the yuan-to-dollar exchange rate, with China accounting for a very high 26% of South Korea’s exports. Reflecting this situation, the Bank for International Settlements’ calculation of the real effective exchange rate (REER) for the won had China accounting for a much larger percentage than the US by a margin of 33% to 14%.

Another factor driving up the won’s value is the increased gap between the South Korean and US real interest rates. South Korea has a higher rate of return on 10-year government bonds than the US, with a lower rate of consumer price inflation. Accordingly, it has continued to maintain a higher real interest rate than the US; as of August, it stood at 0.71%, 1.39 percentage points higher than the US rate of -0.67%.

At the same time, South Korea’s current account remains in surplus conditions. While the rate is seen as very likely to decline to around 3.5% of GDP this year from as high as 7.2% in 2015, the current account surplus itself remains in place. The reason has to do with the total savings rate, which exceeds the total domestic investment rate for the South Korean economy.

While the exchange rate influences economic growth through imports and exports, it is also closely tied to stock prices. An analysis of figures since 1998 showed a correlation coefficient of -0.42 between the won-to-dollar exchange rate and KOSPI stock prices. This means that stock prices have tended to rise whenever the value of the won has increased. In the long term, a tandem rise in the won’s value and stock prices appears very likely.

By Kim Young-ick, adjunct professor of economics at Sogang University

Please direct comments or questions to [english@hani.co.kr]

Editorial・opinion

![[Editorial] Does Yoon think the Korean public is wrong?](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/original/2024/0417/8517133419684774.jpg "[Editorial] Does Yoon think the Korean public is wrong?") [Editorial] Does Yoon think the Korean public is wrong?

[Editorial] Does Yoon think the Korean public is wrong?![[Editorial] As it bolsters its alliance with US, Japan must be accountable for past](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/original/2024/0417/6817133413968321.jpg "[Editorial] As it bolsters its alliance with US, Japan must be accountable for past") [Editorial] As it bolsters its alliance with US, Japan must be accountable for past

[Editorial] As it bolsters its alliance with US, Japan must be accountable for past- [Guest essay] Amending the Constitution is Yoon’s key to leaving office in public’s good graces

- [Editorial] 10 years on, lessons of Sewol tragedy must never be forgotten

- [Column] A death blow to Korea’s prosecutor politics

- [Correspondent’s column] The US and the end of Japanese pacifism

- [Guest essay] How Korea turned its trainee doctors into monsters

- [Guest essay] As someone who helped forge Seoul-Moscow ties, their status today troubles me

- [Editorial] Koreans sent a loud and clear message to Yoon

- [Column] In Korea’s midterm elections, it’s time for accountability

Most viewed articles

- 1‘Right direction’: After judgment day from voters, Yoon shrugs off calls for change

- 2[Editorial] Does Yoon think the Korean public is wrong?

- 3[Editorial] As it bolsters its alliance with US, Japan must be accountable for past

- 4Where Sewol sank 10 years ago, a sea of tears as parents mourn lost children

- 5Strong dollar isn’t all that’s pushing won exchange rate into to 1,400 range

- 6[Guest essay] Amending the Constitution is Yoon’s key to leaving office in public’s good graces

- 7Japan officially says compensation of Korean forced laborers isn’t its responsibility

- 8[News analysis] Watershed augmentation of US-Japan alliance to put Korea’s diplomacy to the test

- 9Korea ranks among 10 countries going backward on coal power, report shows

- 10US, Japan and China move to become self-sufficient in semiconductors