hankyoreh

Links to other country sites 다른 나라 사이트 링크

Chaebol owners owning less but controlling more

By Kwak Jung-soo, senior staff reporter

Data show an average stake of less than 1% among owners of the top ten South Korean conglomerates (chaebol) for the first time in history, as well as a combined internal possession rate in the low 50% range for family members and affiliates.

The numbers are expected to prompt stronger calls for conglomerate reform by civic groups and politicians on both sides of the aisle ahead of December’s presidential election.

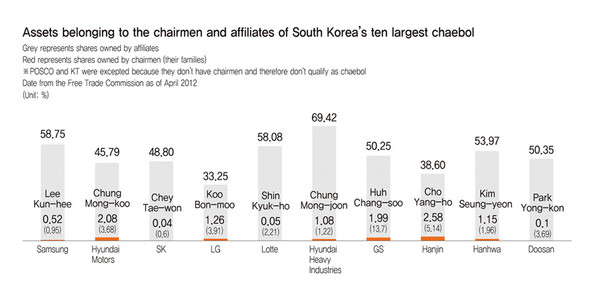

On July 1, the Fair Trade Commission announced stock holding rates for conglomerates with assets of 5 trillion won (US$4.37 billion) or more. The average rate of ownership by an owner for the top ten conglomerates that had one, including Samsung and Hyundai Motors, stood at 0.94% as of April, down 0.16 percentage points from last year.

The percentage had been steadily dwindling since 1990, when it stood at 5.1%, before steadying at just above 1% over the past five years.

At the same time, the internal ownership rate for the top ten conglomerates rang in at 55.73%, up 2.23 percentage points from a year prior and the highest level since 1990, when the rate was 56.2%.

The numbers indicate a widening gulf between conglomerate ownership and control, as owners gain a tighter grip through their affiliate stakes despite their reduced ownership. The smallest stake for a conglomerate owner among the top ten was SK chairman Chey Tae-won’s 0.04%. Lee Kun-hee, chairman at top-ranked Samsung, owned a share of just 0.52%.

The internal possession rate for the 43 conglomerates with an owner and 5 trillion won or more in assets averaged 56.1%, a 1.9 percent increase from 2011. While the share of owners was down 0.1 percent to 2.13%, their affiliate ownership was up 2.2 percent to 49.6%.

For 1,349 of the 1,565 affiliates at the 43 conglomerates, or 86.2%, the owner did not hold any shares at all.

“The fact that overall internal possession has increased despite the drop in the owner’s stake can be interpreted as showing a deepening divide between possession and control,” said FTC competition policy bureau chief Jeong Jung-won.

“The danger still exists of owners seeking personal gains and making incursions into the territory of SMEs,” Jeong added.

Owners at 29 of the 43 conglomerates that had one were found to be holding shares at a total of 139 finance- and insurance-related affiliates. Not including financial groups, conglomerates like Samsung, Lotte, and Dongbu were found to have large numbers of such affiliates -- eleven for the first and ten each for the latter two. Sixty of these affiliates showed an average of 23.82% invested in equity at 149 other affiliates with customer money. For instance, Samsung Life Insurance had a 6.5% stake in Samsung Electronics and a 4.7% stake in Samsung C&T.

The FTC also unveiled a graphic laying out the complex investment structure at conglomerates. The 43 conglomerates with owners were found to have an average of 4.4 stages of investment, including a number of examples of horizontal and radial investment. Some fifteen conglomerates, including Samsung and Hyundai Motors, were shown to have circular shareholding among affiliates.

The twenty conglomerates without owners, which included public enterprises, were found to have a much simpler ownership structure, with an average of just 1.8 investment stages.

The 43 conglomerates with owners had 230 listed affiliates, amounting to 14.7% of the total. Organizational investors owned 17.8% of these affiliates, while foreign investors owned 16.2%. Combined, their total share of 34% was smaller than the 40.1% internal ownership rate, leaving them unable to exert much control.

Economic Reform Research Institute (ERRI) analyst Wi Pyung-ryang stressed the need to legislate conglomerate reform measures.

“If we are going to prevent owners from controlling an entire conglomerate with just a piddling share of it, we need to amend the Fair Trading Act to ban circular equity investment, and we need to strengthen the role of pensions and other organizational investors to prevent management abuses by the owners,” Wi said.

Wi also stressed the need to keep finance and industry separate in order to prevent the conglomerate owners from using affiliate customer money to maintain and increase their own control.

Please direct questions or comments to [english@hani.co.kr]

Editorial・opinion

![[Column] Has Korea, too, crossed the Rubicon on China?](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/original/2024/0419/9317135153409185.jpg "[Column] Has Korea, too, crossed the Rubicon on China?") [Column] Has Korea, too, crossed the Rubicon on China?

[Column] Has Korea, too, crossed the Rubicon on China?![[Correspondent’s column] In Japan’s alliance with US, echoes of its past alliances with UK](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/original/2024/0419/2317135166563519.jpg "[Correspondent’s column] In Japan’s alliance with US, echoes of its past alliances with UK") [Correspondent’s column] In Japan’s alliance with US, echoes of its past alliances with UK

[Correspondent’s column] In Japan’s alliance with US, echoes of its past alliances with UK- [Editorial] Does Yoon think the Korean public is wrong?

- [Editorial] As it bolsters its alliance with US, Japan must be accountable for past

- [Guest essay] Amending the Constitution is Yoon’s key to leaving office in public’s good graces

- [Editorial] 10 years on, lessons of Sewol tragedy must never be forgotten

- [Column] A death blow to Korea’s prosecutor politics

- [Correspondent’s column] The US and the end of Japanese pacifism

- [Guest essay] How Korea turned its trainee doctors into monsters

- [Guest essay] As someone who helped forge Seoul-Moscow ties, their status today troubles me

Most viewed articles

- 1[Column] The clock is ticking for Korea’s first lady

- 2Samsung barricades office as unionized workers strike for better conditions

- 3[Editorial] When the choice is kids or career, Korea will never overcome birth rate woes

- 4S. Korea, Japan reaffirm commitment to strengthening trilateral ties with US

- 5[News analysis] After elections, prosecutorial reform will likely make legislative agenda

- 6Japan officially says compensation of Korean forced laborers isn’t its responsibility

- 7[Editorial] As it bolsters its alliance with US, Japan must be accountable for past

- 8[Editorial] Does Yoon think the Korean public is wrong?

- 9Why Israel isn’t hitting Iran with immediate retaliation

- 10[Interview] Learning about the Sewol tragedy through BTS